Initiating Coverage | NBFC

July 07, 2017

L&T Finance Holdings Ltd

BUY

CMP

`149

Prudent downsizing for attractive business revival

Target Price

`179

L&T Finance Holdings Ltd (LTFH), promoted by L&T Ltd (64.2%) is a leading

Investment Period

12 Months

NBFC with a diversified lending portfolio. Over the last one year the

management has restructured its business model and is focusing on selective

segments where it has competitive advantage, simultaneously downsizing

Sector

NBFC

some products which were making losses.

Market Cap (` cr)

27,181

Range of offerings across diversified book: LTFH’s lending operations are

Beta

1.8

focused on three primary segments viz. Rural 15% (Micro Finance, 2Wheeler

52 Week High / Low

151/74

& Tractors), Housing 19% (Home Loans, LAP & Builder loans) and Wholesale

Avg. Daily Volume

37,68,991

finance 62% (Renewable Energy, Operating Roads, etc.) of loan book. While

Face Value (`)

10

the above segments will be the growth drivers, the management has started

downsizing unattractive range of products.

BSE Sensex

31,369

Loan growth to remain fairly strong: We expect MFI, 2W and Tractor loans to

Nifty

9,675

report 25%/20%/10% CAGR over FY2017-20E respectively. LTFH has been

Reuters Code

LTFH.NS

gaining market share in the Tractor segment (9.5% in 2HFY2017 v/s. 4.5%

Bloomberg Code

LTFH.IN

in 1HFY2017) and expects to achieve double digit over next one year. The

home loan segment is expected to grow at 30% CAGR, while wholesale loan

book by 11% over the same period. The management intends to undertake

Shareholding Pattern (%)

sale down of assets post origination, which will release capital in addition to

Promoters

64.2

strong fee income.

Credit cost should moderate going ahead: LTFH has provided `1,150cr on

MF / Banks / Indian Fls

8.3

its impaired assets and additional `650cr is to be provided. However, there

FII / NRIs / OCBs

16.6

is goodwill on consolidation of its subsidiaries, hence the company will claim

Indian Public / Others

10.9

tax benefit on amortization of the same, which will be used for making

additional provisions, thus, overall credit cost will remain moderate.

Exiting of loss making business to revive ROE: LTFH has restructured some

Abs.(%)

3m 1yr 3yr

business segments and has been downsizing range of products which were

Sensex

4.2

16.2

15.0

loss making. However, as management intends to completely exit the

defocused products, its impact is unlikely to be there from FY19 onwards,

L&T Fin

20.2

63.7

93.5

this together with favorable change in loan book and resultant NIM should

propel the ROE to 17.9% by FY20 from 13.8% in FY17.

Ability to generate strong fee income will support earnings: LTFH has been a

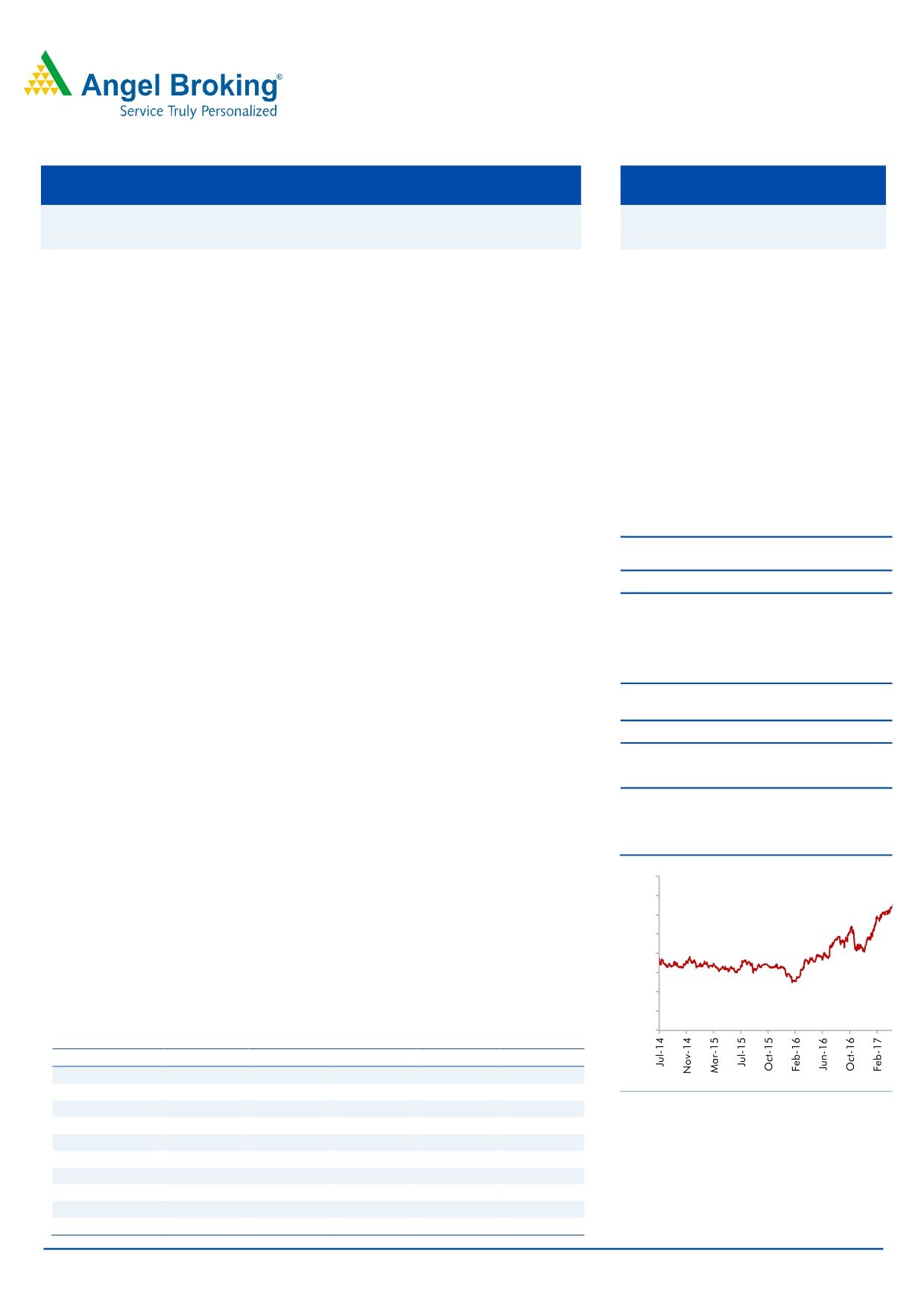

3-year price chart

leader in lending to renewable energy sector and it intends to capitalize on

its expertise of loan origination and subsequently selling it to other financial

160

institutions for fee income. We expect fee income to grow by 30% CAGR over

140

FY2017-20 and this should support a 24% PAT CAGR over the same period.

120

Outlook & Valuation: As LTFH operates in multiple segments, we have

100

valued it based on SOTP. We have valued the rural finance segment at 2.5x,

80

while the housing finance and wholesale finance has been valued at 3x and

60

2x its FY2020E BV each. LTFH’s AMC arm, L&T MF has been valued at 5% of

40

average AUM. Accordingly, we have arrived at a fair value of `179 based

20

on SOTP, and hence recommend BUY on the stock.

0

Key financials (Consolidated)

Y/E March (` cr)

FY2016

FY2017

FY2018E

FY2019E

FY2020E

NII

3,165

3,714

4,006

4,552

5,181

% chg

20.4

17.3

7.9

13.6

13.8

Source: Company, Angel Research

Net profit

854

1,043

1,210

1,520

2,006

% chg

20.8

22.1

16.1

25.6

32.0

NIM (%)

6.0

6.1

5.6

5.5

5.4

EPS (`)

4.9

5.9

6.9

8.7

11.4

P/E (x)

30.4

24.9

21.5

17.1

12.9

Siddharth Purohit

P/BV (x)

3.6

3.3

2.8

2.5

2.2

022 - 3935 7800 Ext: 6872

RoA (%)

1.6

1.7

1.7

1.9

2.1

RoE (%)

11.9

13.8

14.1

15.5

17.9

Source: Company, Angel Research; Note: CMP as of July 06, 2017

Please refer to important disclosures at the end of this report

1

L&T Finance Holdings | Initiating Coverage

Company Background:

L&T Finance Holdings Ltd, promoted by L&T Ltd (holds 64.2%) is a leading

NBFC with a diversified lending portfolio. The NBFC had built a line of

multiple product portfolios, however some of the segments where it didn’t have

significant presence, and was facing severe competition started making losses,

and hence, the management decided to restructure its business model by

downsizing the low profit/ loss making segments. Going ahead, the

management intends to focus only on three segments i.e. Rural Finance,

Housing Finance and Wholesale Finance. The defocused loan book as % of

total loan book has already been brought down to 4% from 8.5%, and we

expect that by FY2018 it will be insignificant compared to the total loan book.

Exhibit 1: Transition towards a more focussed organisation

BEFORE STRATEGY - LTFH 1.0

AFTER STRATEGY - LTFH 2.0

Aspirations of Bank

Aspirations of becoming top quartile NBFC

No RoE focus

Sole objective is RoE focus -18%

Doing 21 products

Doing 7 products in a focused manner

Doing business through 7 lending entities

Doing business through 4 lending entities and shrinking further

Focused on increasing fees along with disbursements

Focused on growing book

Down selling book

Falling short of provisions

Focused on insulating Balance sheet through proactive provisioning

Cost to Income highest at 33%

Cost to Income reduced to 26%

Source: Company, Angel Research

Key Management Personnel:

Mr Dinanath Dubhashi - Managing Director & CEO. He has over 26 years of

experience in the BFSI space involving Corporate Banking, Cash Management,

Credit Ratings, Retail Lending and Rural Finance. He has been associated with

reputed organizations like BNP Paribas, SBI Caps and CARE.

Mr Kailash Kulkani - Chief Executive, Investment Management. He has over 26

years of experience having worked for organizations like Kotak Mahindra AMC,

Met Life and ICICI.

Mr Sunil Prabhune - Chief Executive, Rural and Consumer Lending. He has over 8

years of experience, having worked with ICICI Bank, GE and ICI.

Mr Virender Pankaj - Chief Executive, Wholesale. He has over 25 years of

experience in the banking space and has worked with SBI.

Mr Srikant J - Chief Executive. He has over 20 years of experience and has worked

with BNP Paribas and Commerz Bank AG.

July 07, 2017

2

L&T Finance Holdings | Initiating Coverage

Transition towards a more balanced portfolio of products

and reducing exposure in loss making segments: LTFH had

aspired to become a bank and accordingly had expanded to as high as 21

products. In some of the segments it was a marginal player, while the cost

associated with those businesses was very high, and hence, those segments were

losing money. However, as a change of strategy the organization has been

focusing only on selective 7 products and the key parameters for getting into any

business will be the ability to generate strong RoE.

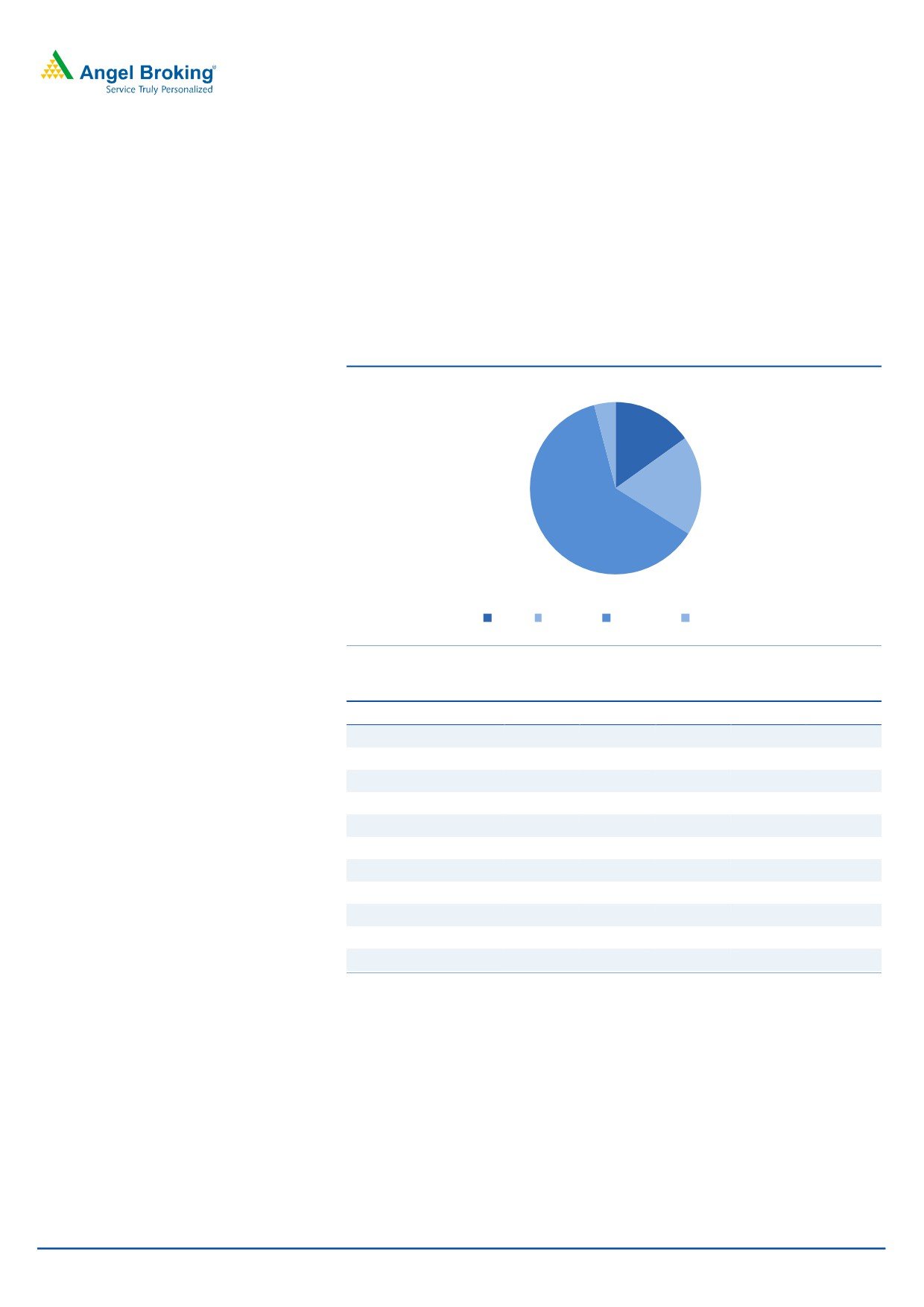

Exhibit 2: Loan Book Composition FY2017 ( % )

4.0

15.1

18.8

62.1

Rural

Housing Wholesale Defocussed

Source: Company, Angel Research

Exhibit 3: Loan Book Composition ( ` Cr )

Segmental Loan Book

FY16

FY17

FY18E

FY19E

FY20E

Rural

8,644

10,041

12,051

14,226

17,077

Housing

9,811

12,534

15,667

19,584

24,480

Wholesale

34,870

41,403

47,200

51,920

57,112

Defocused

4,931

2,671

1,335

668

334

Total

58,256

66,648

76,253

86,398

99,002

Segmental Contribution

Rural

14.8

15.1

15.8

16.5

17.2

Housing

16.8

18.8

20.5

22.7

24.7

Wholesale

59.9

62.1

61.9

60.1

57.7

Defocused

8.5

4.0

1.8

0.8

0.3

Total

100

100

100

100

100

Source: Company, Angel Research

July 07, 2017

3

L&T Finance Holdings | Initiating Coverage

Investment Rationale

Knowledge of rural hinterland coupled with strong OEM

and dealer relationship a key strength of LTFH

The rural finance of LTFH is largely focused on three segments viz. Microfinance

(MFI), Two Wheeler (2W) & Tractors. Over the years LTFH has developed strong

understanding of the rural hinterland, which helps in growing its MFI business.

Further, it has developed excellent relationship with all major OEMs and dealers,

which has been the key differentiator in market share gain in the 2W and Tractor

financing segments. It has also strengthened the collection systems over the years,

which is critical as far as long term sustainability of this business is concerned.

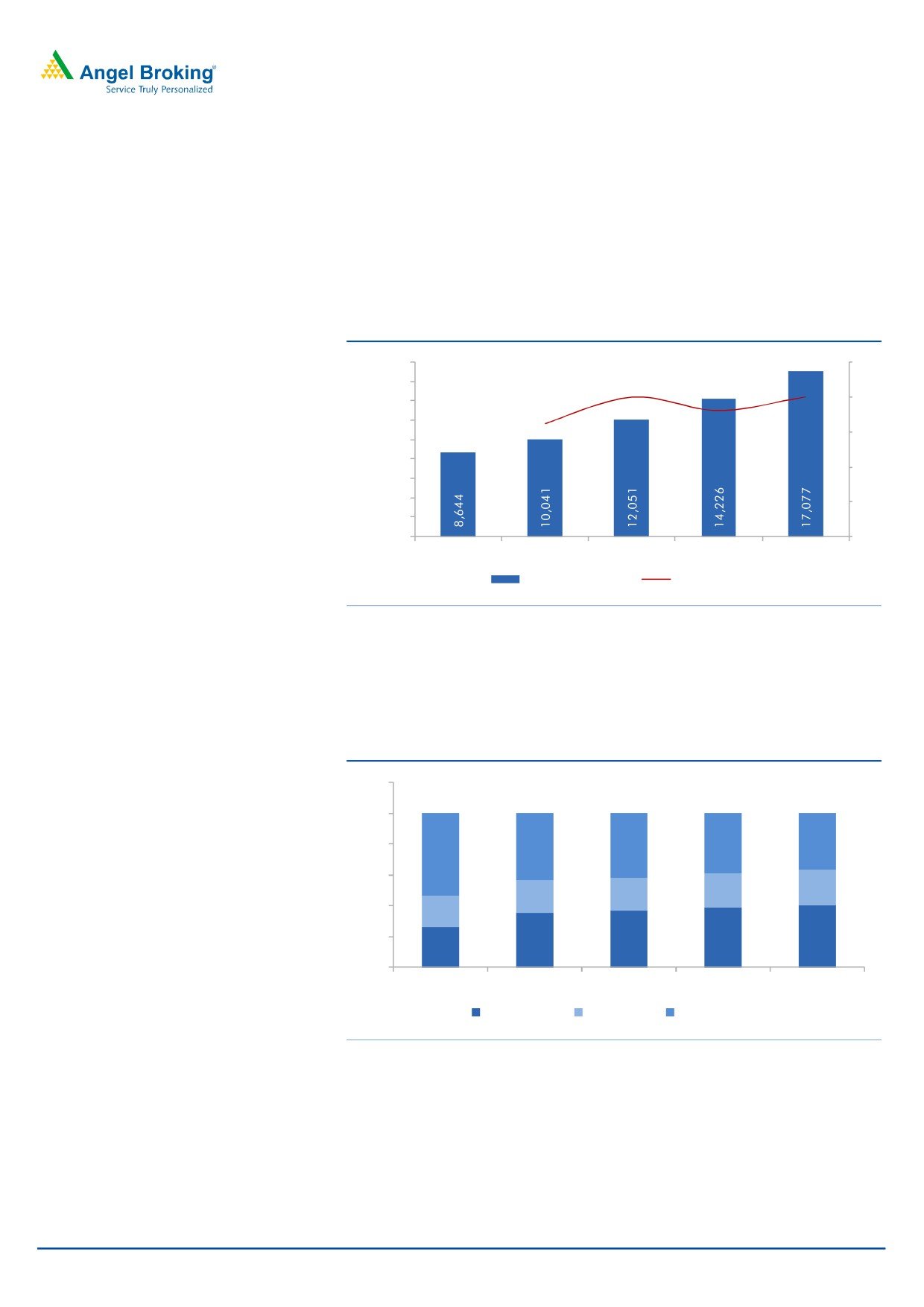

Exhibit 4: Rural loan growth product wise

` Cr

FY16

FY17

FY18E FY19E FY20E

Micro Finance

2,234

3,551

4,439

5,548

6,936

% Change YoY

-

59

25

25

25

2W Finance

1,761

2,110

2,532

3,089

3,800

% Change YoY

-

20

20

22

23

Farm Equipment

4,649

4,379

5,080

5,588

6,342

% Change YoY

-

(6)

16

10

14

Total

8,644

10,041

12,051

14,226

17,077

Source: Company, Angel Research

Microfinance will continue to be a growth driver in rural segment: Microfinance

business has been a growth driver for LTFH growing by 59% in FY2017. While

there has been some moderation in the last two quarters, we expect MFI book to

grow at 25% CAGR over FY2017-20 and account for 41% of the total rural loan

book. The company has been quick in adapting to technology for the segment,

and has now migrated to 100% cashless and ‘Adhar’ based disbursements.

Two Wheelers segment leaves scope for further market share gain: LTFH has

adopted technology and algorithm based database, which has resulted in sharp

improvement in turnaround time. Ability to take credit call within 10 minutes vis-à-

vis few hours has enabled it to grow this book and gain market share. We expect

the 2W loans to grow by 20% CAGR over FY2017-20 and account for 23% of the

total 2W loan book by FY2020.

Emerging as market leader in the tractor segment: The tractor segment depends a

lot on factors like income levels in rural economy, monsoon and also on various

program of Government addressing the rural masses. Despite lot of moving

factors, LTFH has gained strong market share in tractor financing backed by

increasing presence and relationship with dealers of top OEMs. The market share

has doubled to 9.5% in 2HFY2017 v/s. 4.5% in 1HFY2017, and the management

is confident of having double digit market share in next few quarters.

July 07, 2017

4

L&T Finance Holdings | Initiating Coverage

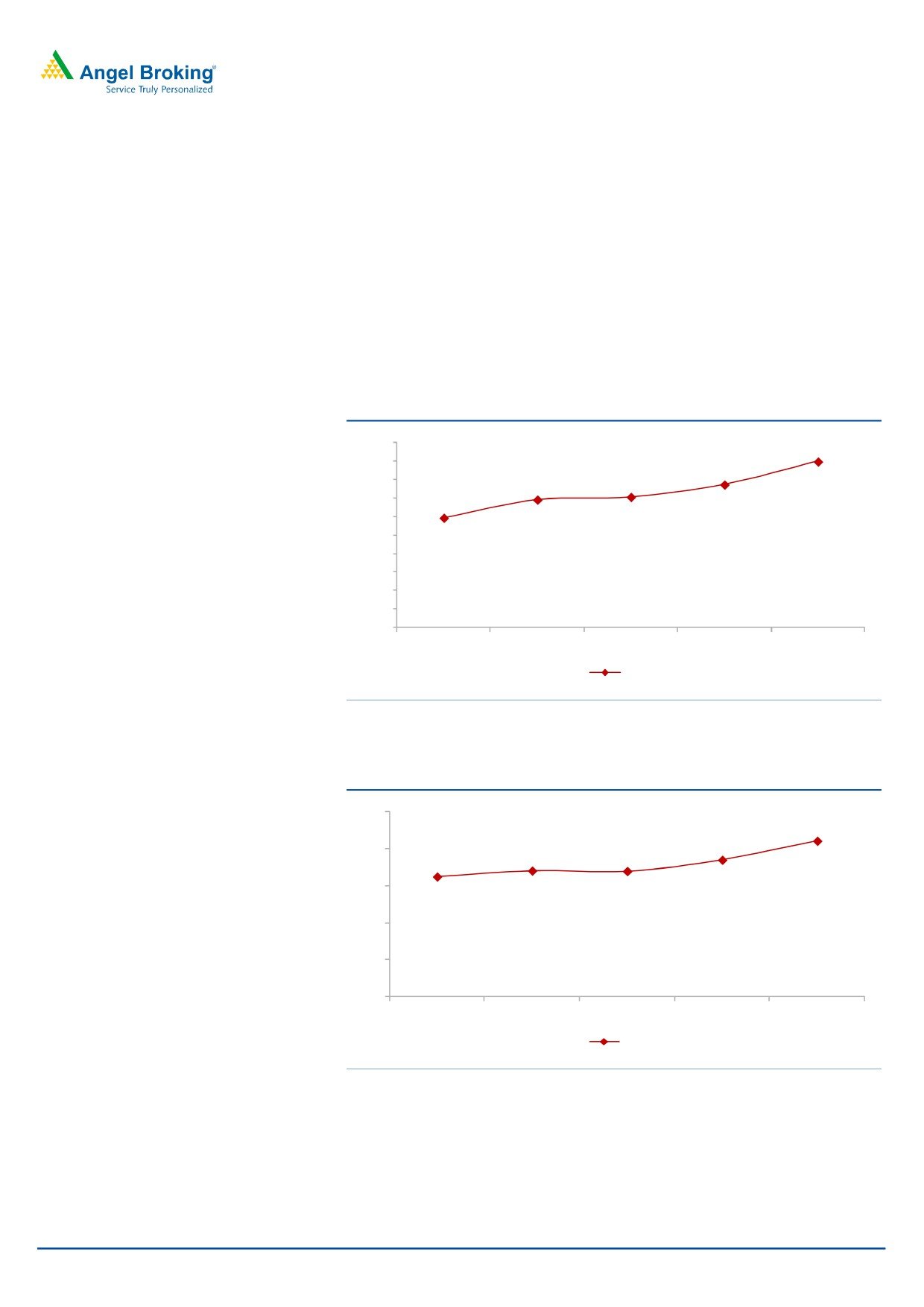

Rural Finance will continue to be a growth driver

Rural segment will continue to be a key area of focus for LTFH. In FY2017 the

company reported 16.2% growth in the rural book. However, the steps taken with

regards to adaptation of technology, faster turnaround time and higher presence

across dealer network could help in growth rate accelerating in the years to come.

We expect 19% CAGR in loan book over FY2017-20.

Exhibit 5: Loan Book growth Rural Business (` Cr)

18,000

25

16,000

20.0

20.0

18.0

20

14,000

16.2

12,000

15

10,000

8,000

10

6,000

4,000

5

2,000

-

0

FY16

FY17

FY18E

FY19E

FY20E

Rural Finance Rs Cr

% Growth YoY

Source: Company, Angel Research

The nature of rural business is of higher credit costs, and hence we have factored

in 450 bps credit cost, similar to FY2017. However, the higher yield should take

care of the credit cost, and despite this the higher operating leverage will ensure

~21% ROE in this business.

Exhibit 6: Rural Loans Composition (%)

120

100

80

39

37

44

42

54

60

22

22

21

21

40

20

20

35

37

39

41

26

0

FY16

FY17

FY18E

FY19E

FY20E

Micro Finance

2W Finance

Farm Equipment

Source: Company, Angel Research

July 07, 2017

5

L&T Finance Holdings | Initiating Coverage

Exhibit 7: Income Statement Rural Business

` Cr

FY16

FY17

FY18E

FY19E

FY20E

Interest Income

1,589

1,823

2,164

2,521

2,964

Interest Cost

611

682

839

946

1,100

Net Interest Income

979

1,141

1,324

1,575

1,864

Fee Income & Other income

70

86

99

114

131

Total Income

1,049

1,227

1,423

1,689

1,995

Total Operating Expenses

390

359

370

400

440

PPP

658

867

1,053

1,289

1,555

Provisions, contingencies & w/off

336

425

497

591

704

PBT

323

443

556

698

851

Tax

112

154

189

237

289

PAT

211

289

367

461

562

Source: Company, Angel Research

Exhibit 8: Balance Sheet

` Cr

FY16

FY17

FY18E

FY19E

FY20E

Closing Gross Loans & Advances

8,644

10,041

12,051

14,226

17,077

Total Assets

9,152

10,412

12,476

14,726

17,727

Closing Net worth

1,193

1,331

1,698

2,158

2,720

Closing Borrowing

7,329

8,686

10,162

11,890

13,911

Other Liabilities

630

396

616

678

1,096

Total Liabilities

9,152

10,412

12,476

14,726

17,727

Source: Company, Angel Research

Exhibit 9: Key Ratios Rural Business

Key Assumptions

FY16

FY17

FY18E

FY19E

FY20E

Growth (% )

Loans

-

16.2

20.0

18.0

20.0

Borrowings

-

18.5

17.0

17.0

17.0

NII

-

16.5

16.1

18.9

18.4

Provisions

-

26.5

17.0

18.9

19.1

PAT

-

37.0

27.2

25.4

22.0

Key Ratios (%)

Yield on advances

20.3

19.8

19.6

19.2

18.9

Cost of funds

9.2

8.6

8.3

8.0

7.9

NIM%

12.5

12.4

12.0

12.0

11.9

Credit Cost

4.3

4.6

4.5

4.5

4.5

ROA

2.4

2.9

3.0

3.2

3.3

ROE

17.7

21.7

21.6

21.3

20.7

Source: Company, Angel Research

July 07, 2017

6

L&T Finance Holdings | Initiating Coverage

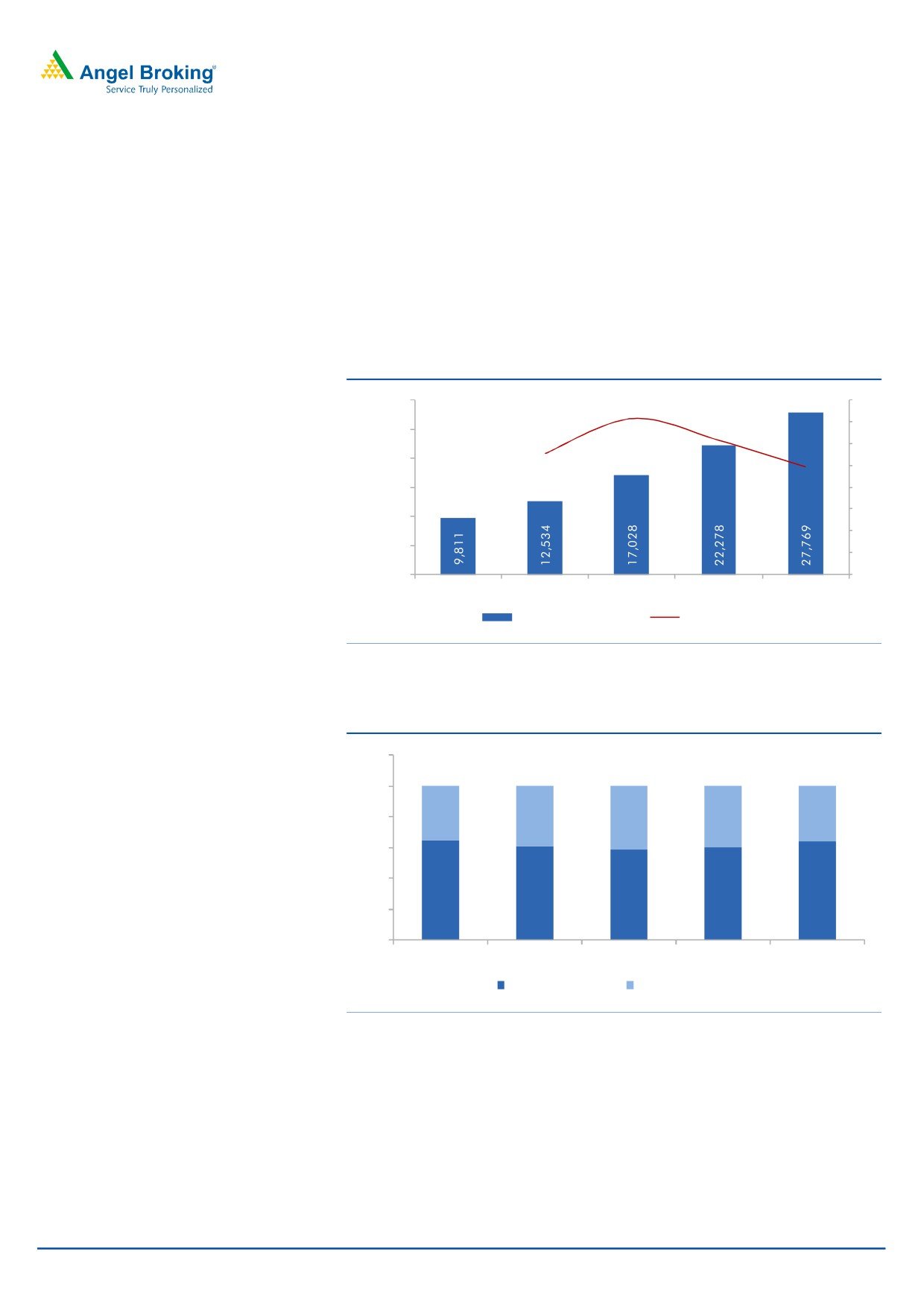

Growth has just begun for Housing Finance segment

LTFH has the potential to become a meaningful player in the housing finance

segment in the years to come. Under this segment it lends to individual home

loans, Loan Against Property (LAP) and also to developers. The segment grew by

27.8% YoY in FY2017 and accounted for 18.8% of the overall loan book. We

expect the overall Housing Finance book to report 30% CAGR over FY2017-20.

Exhibit 10: Segmental Growth Housing Loans

` Cr

FY16

FY17

FY18E

FY19E

FY20E

Retail Home Loans / LAP

6,313

7,643

9,936

13,413

17,840

% Change YoY

21.1

30.0

35.0

33.0

Real Estate Finance

3,498

4,891

7,092

8,865

9,929

% Change YoY

39.8

45.0

25.0

12.0

Total

9,811

12,534

17,028

22,278

27,769

% Growth YoY

27.8

35.9

30.8

24.6

Source: Company, Angel Research

Retail home loans/ LAP segment to see further improvement in traction: The retail

home loan segment of LTFH caters to both salaried as well non salaried-self

employed segments. However, as the margins in salaried segment are relatively

lower, hence, in order to improve its overall NIMs, the company intends to

increasingly focus more on the non salaried segment, which faces less competition

as well as offers better yield. LAP accounts for ~33% of the individual home loans

segment.

Builder’s loan segment could aid higher margins in the Housing Finance segment:

In FY2017, the loans book towards developers reported a strong growth of ~40%.

In the developer loan segment LTFH will use parent L&T domain expertise, which

will be used as the key mover for growing the housing finance space. Currently

also, the company is lending only to the Tier 1 builders after doing lot of due

diligence. While on one hand, it will lend to the developers, it will also generate

leads from the same set of developers for its retail home loans, thus enhancing its

cross selling capability.

Higher incremental business from developer loans and self employed segment

should be RoE accretive: Generally, the fee income from developer loans are

higher compared to other retail loans. Though developer loans will continue to

grow at a healthy pace its share in total loans is expected to come down gradually.

And as a result of better spread and higher fee income this is likely to result in a

sustainable 20% ROE for the segment, despite increasing competition in the retail

loans space. Further, in the home loans to the salaried segment, incrementally the

company is relying more on its own origin rather than sourcing from DSA, which

should result in lower cost.

July 07, 2017

7

L&T Finance Holdings | Initiating Coverage

AUM growth to be higher than industry growth in Housing

Finance segment

The Housing Finance segment reported a 27.8% growth in AUM in FY2017 and

we expect it to report a 30% CAGR over FY2017-20, backed by 26% and 36%

growth in Home Loans/ LAP and Developer loan segment respectively. We have

factored in a marginally higher credit cost, as the share of loans from the non

salaried segment goes up for the segment, and hence expect the PAT CAGR of

25% over the same period.

Exhibit 11: Growth in Housing Finance

30,000

35.9

24.6

40

30.8

35

25,000

27.8

30

20,000

25

15,000

20

15

10,000

10

5,000

5

-

0

FY16

FY17

FY18E

FY19E

FY20E

Housing Finance Rs Cr

% Growth YoY

Source: Company, Angel Research

Exhibit 12: Loan Bifurcation Housing Finance Segment (%)

120

100

80

36

39

36

42

40

60

40

64

61

58

60

64

20

0

FY16

FY17

FY18E

FY19E

FY20E

Home Loans / LAP

Real Estate Finance

Source: Company, Angel Research

July 07, 2017

8

L&T Finance Holdings | Initiating Coverage

Exhibit 13: Income statement Housing Loans

` Cr

FY16

FY17

FY18E

FY19E

FY20E

Interest Income

941

1,386

1,733

2,122

2,597

Interest Cost

604

832

1,100

1,332

1,611

Net Interest Income

338

554

633

790

986

Fee Income & Other income

45

90

113

138

168

Total Income

383

644

746

928

1,154

Total Operating Expenses

156

157

173

190

209

PPP

227

487

573

738

945

Provisions, contingencies & w/off

26

68

78

109

143

PBT

201

420

495

628

802

Tax

73

146

168

214

273

PAT

128

274

327

415

529

Source: Company, Angel Research

Exhibit 14: Balance Sheet Housing Finance

` Cr

FY16

FY17

FY18E

FY19E

FY20E

Closing Gross Loans & Advances

9,811

12,534

15,667

19,584

24,480

Total Assets

10,615

13,220

16,387

20,334

25,305

Closing Net worth

991

1,363

1,690

2,104

2,634

Closing Borrowing

8,829

11,115

13,782

17,227

21,534

Other Liabilities

1,786

2,106

2,605

3,107

3,771

Total Liabilities

10,615

13,220

16,387

20,334

25,305

Source: Company, Angel Research

Exhibit 15: Key Ratios Housing Finance Business

Key Assumptions

FY16

FY17

FY18E

FY19E

FY20E

Growth (% )

Loans

-

27.8

37.0

29.3

25.0

Borrowings

-

25.9

24.0

25.0

25.0

NII

-

64.0

14.2

24.8

24.8

Provisions

-

162.9

14.7

40.9

31.0

PAT

-

113.2

19.5

26.9

27.6

Key Ratios (%)

Yield on advances

12.2

12.4

12.3

12.0

11.8

Cost of funds

8.8

8.4

8.0

7.7

7.5

NIM%

4.4

5.0

4.5

4.5

4.5

Credit Cost

0.3

0.6

0.6

0.6

0.7

ROA

1.3

2.2

2.1

2.1

2.2

ROE

12.9

20.1

19.3

19.7

20.1

Source: Company, Angel Research

July 07, 2017

9

L&T Finance Holdings | Initiating Coverage

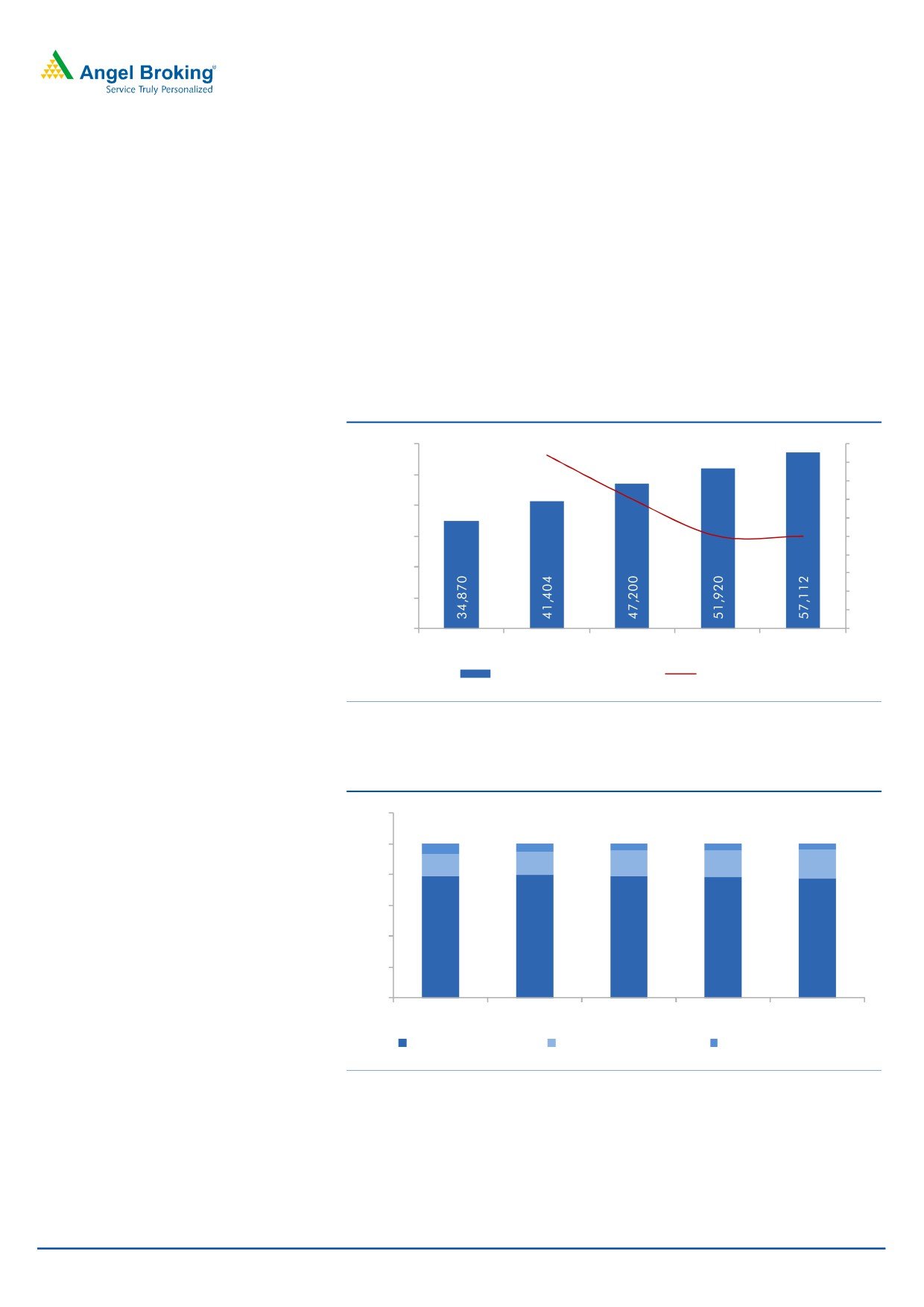

Wholesale finance to generate high fee income

The wholesale finance segment reported a 18.7% growth in AUM in FY2017 and

we expect it to report 11% CAGR over FY2017-20. The key strategy in wholesale

finance will be to originate the deal and sell the assets to other financial institutions

for some fees. LTFH is already a pioneer in lending to the renewable energy sector

and intends to capitalize on the domain knowledge it has developed over the years

in funding to the new sector where there is limited competition. Further, it also has

been financing to operating roads and transmission sectors within the wholesale

finance business.

Exhibit 16: Loan Bifurcation - Wholesale Finance

` Cr

FY16

FY17

FY18E

FY19E

FY20E

Infrastructure Finance

27,604

32,884

37,134

40,476

44,119

% Growth YoY

-

19.1

12.9

9.0

9.0

Structured Corp Finance

4,979

6,397

7,932

9,281

10,766

% Growth YoY

-

28.5

24.0

17.0

16.0

Supply Chain Finance

2,287

2,123

2,134

2,163

2,227

% Growth YoY

-

(7.2)

0.5

1.4

3.0

Total

34,870

41,404

47,200

51,920

57,112

% Growth YoY

-

18.7

14.0

10.0

10.0

Source: Company, Angel Research

Exhibit 17: Loan Composition of Wholesale Finance

5%

Renewables

15%

31%

Transport

Power-Thermal

Power- Corporate+T&D

14%

Others

7%

19%

8%

Structured Corp Finance

Supply Chain Finance

Source: Company, Angel Research

July 07, 2017

10

L&T Finance Holdings | Initiating Coverage

Sale down of assets will ensure higher bottom-line growth

with low capital consumption

LTFH, on the back of its strong parentage has developed strong domain

knowledge of financing the large and long gestation projects. While the assets

financed before 2011 have lot of stress, those after 2011 have been strong in

balance sheet. Going ahead, the management intends to sale down assets after

strong underwriting process. Projects which are financed have a strong cash flow

potential, and hence LTFH intends to generate strong fee income out of selling the

loans. There is strong demand for this type of transactions both from Banks and

other NBFCs.

Exhibit 18: Loan growth in Wholesale finance

18.7

60,000

20

18

14.0

50,000

16

10.0

14

40,000

10.0

12

30,000

10

8

20,000

6

4

10,000

2

-

0

FY16

FY17

FY18E

FY19E

FY20E

Wholesale Finance ( Rs Cr )

% Growth YoY

Source: Company, Angel Research

Exhibit 19: Wholesale Finance Loan Composition (%)

120

100

7

5

5

4

4

14

15

17

18

19

80

60

40

79

79

79

78

77

20

0

FY16

FY17

FY18E

FY19E

FY20E

Infrastrcature Finance

Structured Corp Finance

Supply Chain Finance

Source: Company, Angel Research

July 07, 2017

11

L&T Finance Holdings | Initiating Coverage

Exhibit 20: Income Statement Wholesale Finance

` Cr

FY16

FY17

FY18E

FY19E

FY20E

Interest Income

3,717

4,064

4,773

5,191

5,547

Interest Cost

2,429

2,736

3,372

3,663

3,953

Net Interest Income

1,288

1,328

1,401

1,528

1,593

Fee Income & Other income

144

299

404

485

582

Total Income

1,432

1,627

1,805

2,013

2,175

Total Operating Expenses

176

159

166

186

209

PPP

1,257

1,469

1,639

1,826

1,966

Provisions, contingencies & w/off

461

712

665

595

545

PBT

795

757

974

1,232

1,421

Tax

247

197

244

320

370

PAT

548

560

731

911

1,052

Source: Company, Angel Research

Exhibit 21: Balance Sheet Wholesale Finance

` Cr

FY16

FY17

FY18E

FY19E

FY20E

Closing Business Assets

34,870

41,403

47,200

51,920

57,112

Total Assets

37,026

44,111

50,124

55,078

60,523

Closing Net worth

4,591

5,316

5,864

6,548

7,337

Closing Borrowing

30,593

37,164

41,996

46,195

50,815

Other Liabilities

1,841

1,630

2,264

2,335

2,371

Total Liabilities

37,026

44,111

50,124

55,078

60,523

Source: Company, Angel Research

Exhibit 22: Key Ratios Wholesale Finance

Key Assumptions

FY16

FY17

FY18E

FY19E

FY20E

Growth (% )

Loans

-

18.7

14.0

10.0

10.0

Borrowings

-

21.5

13.0

10.0

10.0

NII

-

3.1

5.5

9.1

4.3

Provisions

-

54.3

(6.7)

(10.5)

(8.3)

PAT

-

2.1

30.5

24.7

15.4

Key Ratios (%)

Yield on advances

11.9

11.0

10.8

10.5

10.2

Cost of funds

8.8

8.4

8.0

7.9

7.8

NIM%

4.1

3.6

3.2

3.1

2.9

Credit Cost

1.5

1.9

1.5

1.2

1.0

ROA

1.6

1.5

1.5

1.8

1.8

ROE

10.7

10.5

11.7

13.3

13.7

Source: Company, Angel Research

July 07, 2017

12

L&T Finance Holdings | Initiating Coverage

Worst in terms of asset quality is over

While the reported GNPA of LTFH is at 4.9%, including the restructured loans the

gross impaired assets is at 9.8%. Large part of the stress is from the legacy assets

financed prior to 2011, while the new assets financed in the wholesale financed

segment have negligible NPAs. Further, incrementally the company’s focus is on retail

space and the granular nature of book will ensure lower slippages and NPAs in turn.

We expect the GNPAs and NNPAs levels to gradually come down to 3.75% and 2%

of the book by FY2020 respectively.

Exhibit 23: Asset Quality (` Cr)

4,000

3,553

3,367

3,296

3,500

3,146

3,000

2,756

2,500

2,144

1,791

1,854

1,895

2,000

1,799

1,500

1,000

500

-

FY16

FY17

FY18E

FY19E

FY20E

GNPAs Rs Cr NNPAs Rs Cr

Source: Company, Angel Research

Exhibit 24: Asset Quality Trend

6.0

4.9

5.0

4.7

5.0

4.0

3.8

3.8

4.0

2.9

3.0

2.5

2.3

2.0

2.0

1.0

0.0

FY16

FY17

FY18E

FY19E

FY20E

GNPAs %

NNPAs %

Source: Company, Angel Research

July 07, 2017

13

L&T Finance Holdings | Initiating Coverage

Overall credit cost should moderate going ahead

The nature of rural finances is of higher credit costs, which will remain high going

ahead as well. Nonetheless, historically the credit cost for housing finance has

always been lower and under control. The credit cost for the wholesale finance had

been higher over the last two years and might remain higher in FY2018 as well,

we expect the same to moderate going ahead. We expect the blended credit cost

to decline to 1.8% by FY2020 from 2.4% in FY2017. Further, LTFH has increased

its provision coverage ratio on the wholesale book and the blended PCR is likely to

further improve going ahead.

Exhibit 25: Segmental Credit Cost (%)

FY16

FY17

FY18E

FY19E

FY20E

Rural Finance

4.28

4.61

4.50

4.50

4.50

Housing Finance

0.33

0.61

0.55

0.62

0.65

Wholesale Finance

1.47

1.92

1.50

1.20

1.00

Blended Credit Cost

1.49

2.60

2.00

1.80

1.20

Source: Company, Angel Research

Exhibit 26: Credit Cost Trend (%)

3.0

2.6

2.5

2.0

2.0

1.8

1.5

1.5

1.2

1.0

0.5

0.0

FY16

FY17

FY18E

FY19E

FY20E

Credit Cost %

Source: Company, Angel Research

July 07, 2017

14

L&T Finance Holdings | Initiating Coverage

Increasing provision should take care of the impaired assets

While the company has already taken extra voluntary provisions with slippages

remaining under control, overall asset quality trend should remain positive going

ahead. LTFH merged two of its 100% subsidiaries with itself and since the

companies were valued at a premium to their book value there was goodwill to the

tune of `3000cr on account of this. Amortization of goodwill is tax deductible

expenditure and the company intends to use this as an extra provision in its books.

Lower PCR was one of the concerns for LTFH’s book, particularly on the wholesale

finance side. However, it has already increased its PCR on the book and we expect

the same to go up further.

Exhibit 27: PCR Trend (%)

50

46.8

46.7

43.8

42.8

45

40

35

30

25

22.2

20

15

10

5

0

FY16

FY17

FY18E

FY19E

FY20E

PCR %

Source: Company, Angel Research

July 07, 2017

15

L&T Finance Holdings | Initiating Coverage

Shift towards higher yielding assets and lower credit cost to

result in RoE improvement

LTFH’s move to scale down its book on certain products which were making losses

and the renewed focus on increasing share of high yielding assets like Rural

Finance and Housing Finance segments have started paying off. Further, it has

already taken voluntary provisions to cover the impaired assets from the wholesale

book. Despite this, it ended FY2017 with a RoE of 13.8% v/s. 11.9% with

4QFY2017 hitting a high of 14.7%. With increasing sale down of assets in the

wholesale book, the fee income will get a boost and this is likely to have positive

impact on the RoE. We expect the blended RoE of LTFH to hit ~18% by FY2020.

Exhibit 28: ROE Trend (%)

20.0

17.9

18.0

15.5

16.0

13.8

14.1

14.0

11.9

12.0

10.0

8.0

6.0

4.0

2.0

0.0

FY16

FY17

FY18E

FY19E

FY20E

ROE

Source: Company, Angel Research

Exhibit 29: ROA Trend (%)

2.5

2.1

1.9

2.0

1.7

1.7

1.6

1.5

1.0

0.5

0.0

FY16

FY17

FY18E

FY19E

FY20E

ROA

Source: Company, Angel Research

July 07, 2017

16

L&T Finance Holdings | Initiating Coverage

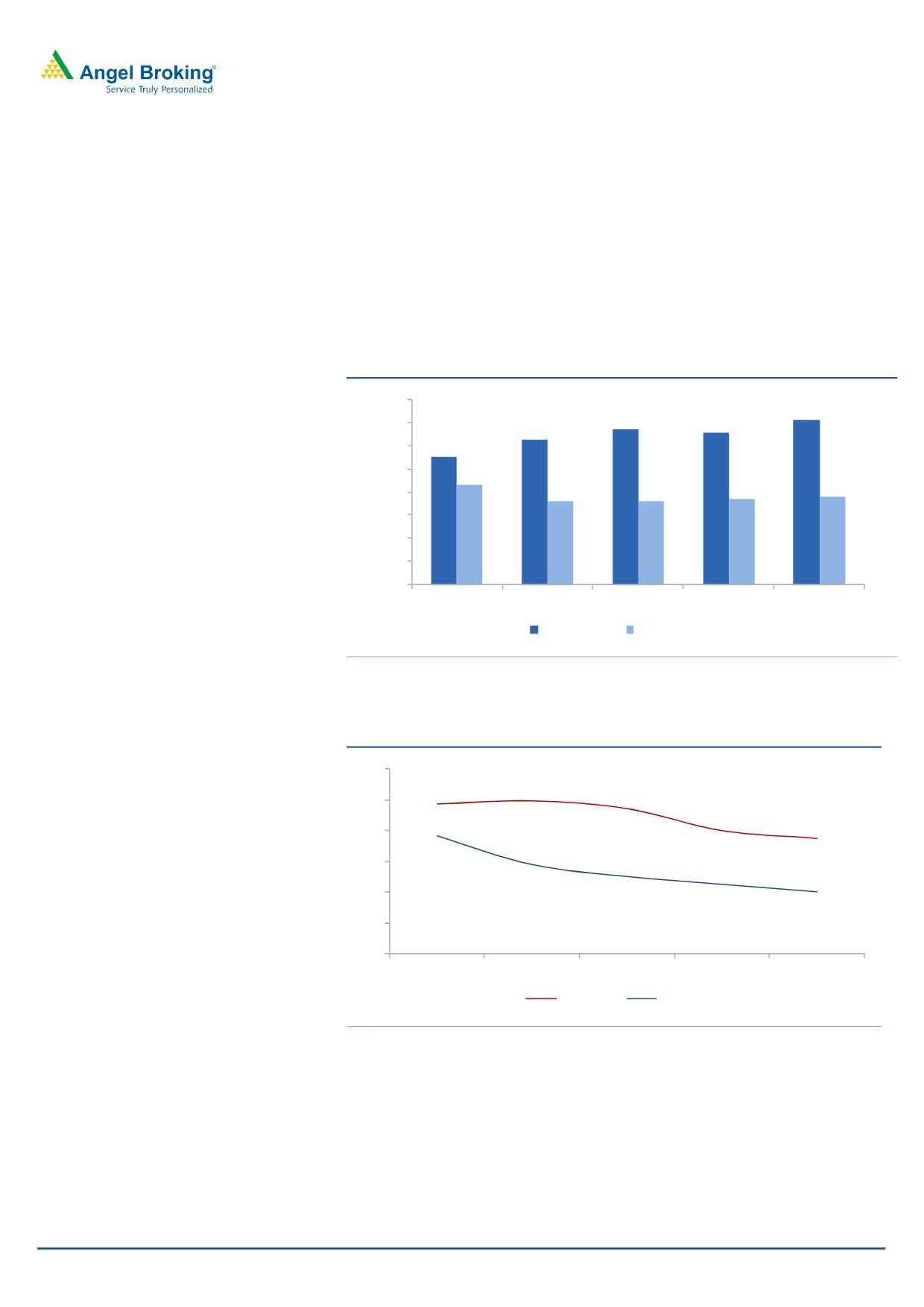

NIM to see marginal drop, still remain healthy: LTFH has historically enjoyed

strong NIM due to its presence in the rural finance segment, which generates

higher yield. While there has been a drop in the blended yield off late, it has also

witnessed reduction in the cost of funds, and hence, NIM improved in FY2017.

However, on conservative basis we have factored in further drop in yield due to

competition in housing finance segment and rural finance segment, where other

NBFCs and Small Finance Banks are also gearing up to scale up aggressively.

Exhibit 30: Yield (%)

Exhibit 31: Cost of funds (%)

15.0

10

8.94

8.50

8.15

8.00

9

7.95

14.5

13.9

8

14.0

13.6

7

13.4

13.5

13.1

6

12.9

5

13.0

4

12.5

3

2

12.0

1

11.5

-

FY16

FY17

FY18E

FY19E

FY20E

FY16

FY17

FY18E

FY19E

FY20E

Yield on assets(%)

Cost of funds (%)

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 32: Spread (%)

Exhibit 33: NIM Trend (%)

6.00

7

5.13

5.23

5.13

6.02

6.07

4.93

4.93

6

5.62

5.55

5.44

5.00

5

4.00

4

3.00

3

2.00

2

1.00

1

-

-

FY16

FY17

FY18E

FY19E

FY20E

FY16

FY17

FY18E

FY19E

FY20E

Spread ( %)

Net Interest Margin(%)

Source: Company, Angel Research

Source: Company, Angel Research

July 07, 2017

17

L&T Finance Holdings | Initiating Coverage

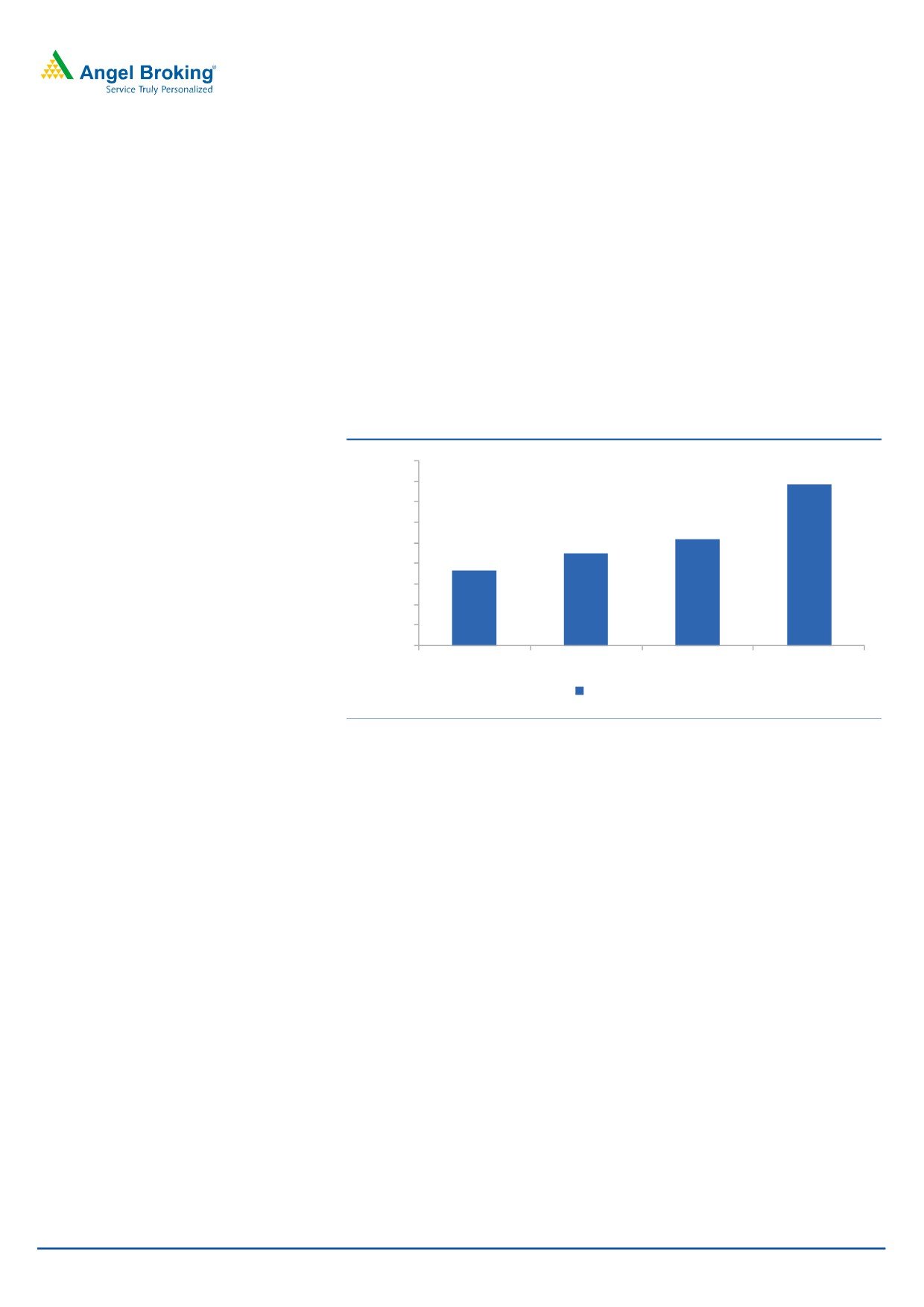

Investment management & wealth management, will aid to the profitability as

well

In 2012, L&T Mutual Fund bought the Indian Operations of Fidelity Mutual

Fund, which had an AUM of ~`8,881cr at that time. Nearly 38% Fidelity’s

total AUM was towards Equity and as a result today also L&T’s overall Equity

exposure in the total AUM at 39% stands higher than industry. In FY17, the

average AUM of L&T AMC has gone up by 51%. While on one hand, it has

been able to increase its AUM, simultaneously it has reduced the costs and

hence, the cost/ income for the investment management business have come

down to 66% by FY2017 from a high of 83% earlier. In FY17, the division

posted PAT of `45cr v/s. `16cr in FY16. Further, the wealth management

segment of the company has also been reporting improved numbers and

reported a PAT of `5cr for FY17 compared to a loss of `24cr in FY16.

Exhibit 34: Increasing AUM (` Cr)

45,000

39,300

40,000

35,000

30,000

25,945

25,000

22,496

18,255

20,000

15,000

10,000

5,000

-

FY14

FY15

FY16

FY17

Average AUM

Source: Company, Angel Research

July 07, 2017

18

L&T Finance Holdings | Initiating Coverage

Outlook and valuation

As LTFH has multiple segments of operations, we have valued it based on SOTP.

We have valued the rural finance segment at 2.5x while the housing finance and

wholesale finance has been valued at 3x and 2x its FY20E BV each. LTFH’s AMC

arm, L&T MF has been valued at 5% of average AUM. Accordingly, we have

arrived at a fair value of `179 based on SOTP, and hence recommend BUY on the

stock.

Exhibit 35: SOTP Valuation

Based on FY20E (` Cr)

Net Worth

Multiple Implied Mkt Cap

Rural

2,694

2.5

6,736

Housing

2,634

3.0

7,901

Whole sale

7,337

2.0

14,674

Combined Value of Lending Business

29,311

Value of MF @ 5% of AUM

1,965

Implied Market Cap

31,276

Implied Per Share

179

CMP

149

% Upside

20%

Source: Company, Angel Research

Exhibit 36: Comparative Valuation & Return ratio

P/BV

RoE%

RoA%

FY17

FY18E

FY19E

FY17

FY18E

FY19E

FY17

FY18E

FY19E

L&T Fin

3.3

2.8

2.5

13.8

14.1

15.5

1.7

1.7

1.9

M&M Fin

2.9

2.6

2.3

7.6

14.7

17.4

1.0

2.0

2.2

Cholamandalam

4.2

3.6

3.1

16.9

18.3

18.9

2.3

2.5

2.6

Shriram City

3.2

2.9

2.5

11.8

15.6

16.6

2.4

3.0

3.0

Magma Fin

1.8

1.7

1.5

1.0

10.5

11.7

0.1

1.5

1.7

REPCO Home

4.6

3.8

3.2

17.6

19.5

20.6

2.4

2.5

2.6

Shriram Transport Fin

2.2

2.0

1.7

11.8

14.1

16.1

1.8

2.2

2.6

Sundaram Fin

3.7

3.5

3.1

15.2

15.6

16.7

2.3

2.4

2.6

Source: Company, Angel Research, Note: CMP as of July 06, 2017, * other NBFCs Consensus taken from Bloomberg,

July 07, 2017

19

L&T Finance Holdings | Initiating Coverage

Exhibit 37: Income Statement ( Consolidated)

` Cr

FY16

FY17

FY18E

FY19E

FY20E

NII

3,165

3,714

4,006

4,552

5,181

- YoY Growth (%)

20.4

17.3

7.9

13.6

13.8

Other Income

182

232

324

422

548

- YoY Growth (%)

28.8

27.4

40.0

30.0

30.0

Operating Income

3,347

3,945

4,330

4,974

5,729

- YoY Growth (%)

20.8

17.9

9.8

14.9

15.2

Operating Expenses

1,313

1,277

1,404

1,545

1,699

- YoY Growth (%)

21.9

-2.8

10.0

10.0

10.0

Pre - Provision Profit

2,034

2,669

2,926

3,430

4,030

- YoY Growth (%)

20.2

31.2

9.7

17.2

17.5

Prov. & Cont.

781

1,590

1,526

1,587

1,492

- YoY Growth (%)

18.0

103.6

(4.0)

4.0

(6.0)

Profit Before Tax

1,253

1,079

1,400

1,843

2,538

- YoY Growth (%)

21.5

(13.9)

29.8

31.6

37.7

Prov. for Taxation

399

36

190

323

531

- as a % of PBT

23.1

(90.9)

422.0

69.9

64.6

PAT

854

1,043

1,210

1,520

2,006

- YoY Growth (%)

20.8

22.1

16.1

25.6

32.0

Source: Company, Angel Research

Exhibit 38: Balance Sheet ( Consolidate)

Y/E March ( ` cr)

FY16

FY17

FY18E

FY19E

FY20E

Share Capital

1,754

1,756

1,820

1,820

1,820

Reserve & Surplus

5,324

6,020

7,433

8,583

10,138

Net Worth

7,195

7,894

9,253

10,403

11,958

Preference Shares

1,213

1,213

1,213

1,213

1,213

Minority Interest

100

119

119

119

119

Borrowings

51,616

59,811

67,935

77,786

89,065

- Growth (%)

15.9

13.6

14.5

14.5

Other Liabilities

2,961

3,035

3,131

3,444

3,789

Total Provisions

645

367

393

422

454

Others

70

75

75

75

75

Total Liabilities

63,801

72,514

82,120

93,463

1,06,672

Cash and Cash equivalents

402

594

654

719

791

Investments

3,563

6,012

6,072

6,375

6,694

Total Loans & Advances

56,065

61,649

71,314

82,058

95,187

- Growth (%)

10.0

15.7

15.1

16.0

Fixed Assets

696

619

631

644

657

Good Will on consolidation

639

639

639

639

639

Others

1,074

1,487

1,509

1,532

1,557

Other Assets

1,361

1,514

1,301

1,496

1,148

Total Assets

63,801

72,514

82,120

93,463

1,06,672

Source: Company, Angel Research

July 07, 2017

20

L&T Finance Holdings | Initiating Coverage

Exhibit 39: Key Ratios ( Consolidated)

FY16

FY17

FY18E

FY19E

FY20E

Profitability ratios (%)

NIMs

6.0

6.1

5.6

5.5

5.4

RoA

1.6

1.7

1.7

1.9

2.1

RoE

11.9

13.8

14.1

15.5

17.9

Asset Quality (%)

Gross NPAs

2,756

3,146

3,352

3,282

3,570

Gross NPAs %

4.9

4.9

4.7

4.0

3.8

Net NPAs

2,144

1,799

1,783

1,846

1,904

Net NPAs %

3.8

2.9

2.5

2.3

2.0

Credit Cost

1.5

2.6

2.0

1.8

1.2

PCR %

22.2

42.8

46.8

43.8

46.7

Per Share Data (`)

EPS

4.9

5.9

6.9

8.7

11.4

BVPS

41.0

45.0

52.7

59.3

68.1

Adj BV

28.8

34.7

42.6

48.8

57.3

DPS

0.8

0.8

1.0

1.8

2.2

Valuation Ratios

PER (x)

30.4

24.9

21.5

17.1

12.9

P/BVPS (x)

3.6

3.3

2.8

2.5

2.2

P/ABVPS (x)

5.1

4.3

3.5

3.0

2.6

Dividend Yield (%)

0.5

0.5

0.7

1.2

1.5

DuPont Analysis

Interest Income

13.9

13.6

13.4

13.1

12.9

Interest Expenses

7.9

7.6

7.8

7.6

7.4

NII

6.0

6.1

5.6

5.5

5.4

Other Inc.

0.3

0.4

0.5

0.5

0.6

Total Income

6.4

6.4

6.1

6.1

6.0

Opex

2.5

2.1

2.0

1.9

1.8

PPP

3.9

4.4

4.1

4.2

4.2

Provision

1.5

2.6

2.1

1.9

1.6

PBT

2.4

1.8

2.0

2.2

2.7

Taxes

0.8

0.1

0.3

0.4

0.6

RoA

1.6

1.7

1.7

1.9

2.1

Leverage

14.6

8.1

8.3

8.3

8.5

RoE

11.9

13.8

14.1

15.5

17.9

Source: Company, Angel Research

July 07, 2017

21

L&T Finance Holdings | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

L&T Finance Holdings Ltd

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)